Compressed Lifecycle is the biggest issue in the sneaker industry (really, it’s sustainability but that’s a different discussion that’s coming). Brands who haven’t decided to chase a weekly drop schedule are seeing the benefits of patience bolstered by disciplined supply chain policies. When a brand chases a number to give investors what they want, versus showing discipline and maintaining a release schedule built around the needs of athletes, those Chase brands over-index on hype as opposed to innovation.

There have always been indicators within resale on how retail should be adjusting. The immediate feedback of a platform like StockX provides readily available insight. The issue is brands work by quarters and months. They can’t actually adjust in real time. This means a company that becomes trendy will undoubtedly produce enough sneakers to satiate fans. In doing so, they commit to a downturn. There is a fine line in refusing to feed the algorithm and missing out on the windfall of cash a hyped product can deliver.

You can’t blame New Balance for pushing 550s into the market, only to have the models sitting discounted on shelves at retail today. New Balance, a private company, may have bought into the hype, but in one of the more balanced models in the sneaker industry, the brand also did incredible work on performance running shoes, marketing and collaborative efforts. New Balance showed… balance. ASICS is currently showing balance. To see this a look into Year over Year data, statements and analysis of sneaker resale is needed.

Year over Year – Sneakers

StockX’s 2024 Report allows for a real discussion on how one platform is explaining what is occurring in sneaker resale. When reading their commentary, it must be framed as a private platform who doesn’t share its revenue, attempting to place a positive spin on a business which has cooled considerably. As a matter of fact, the first part of this series shows how StockX has adjusted to a slow resale market:

If there wasn’t an issue in resale would these adjustments have been made? Especially the addition of Google AdSense? Here are two quotes showing a year over year brief on the brands doing well on StockX. I’ve added notes in red on the reality of the statements and an explanation of why the information must be carefully considered. (The information is strictly for the U.S. Information on other regions can be requested by consultation, cburns@arch-usa.com)

What StockX said in June 23:

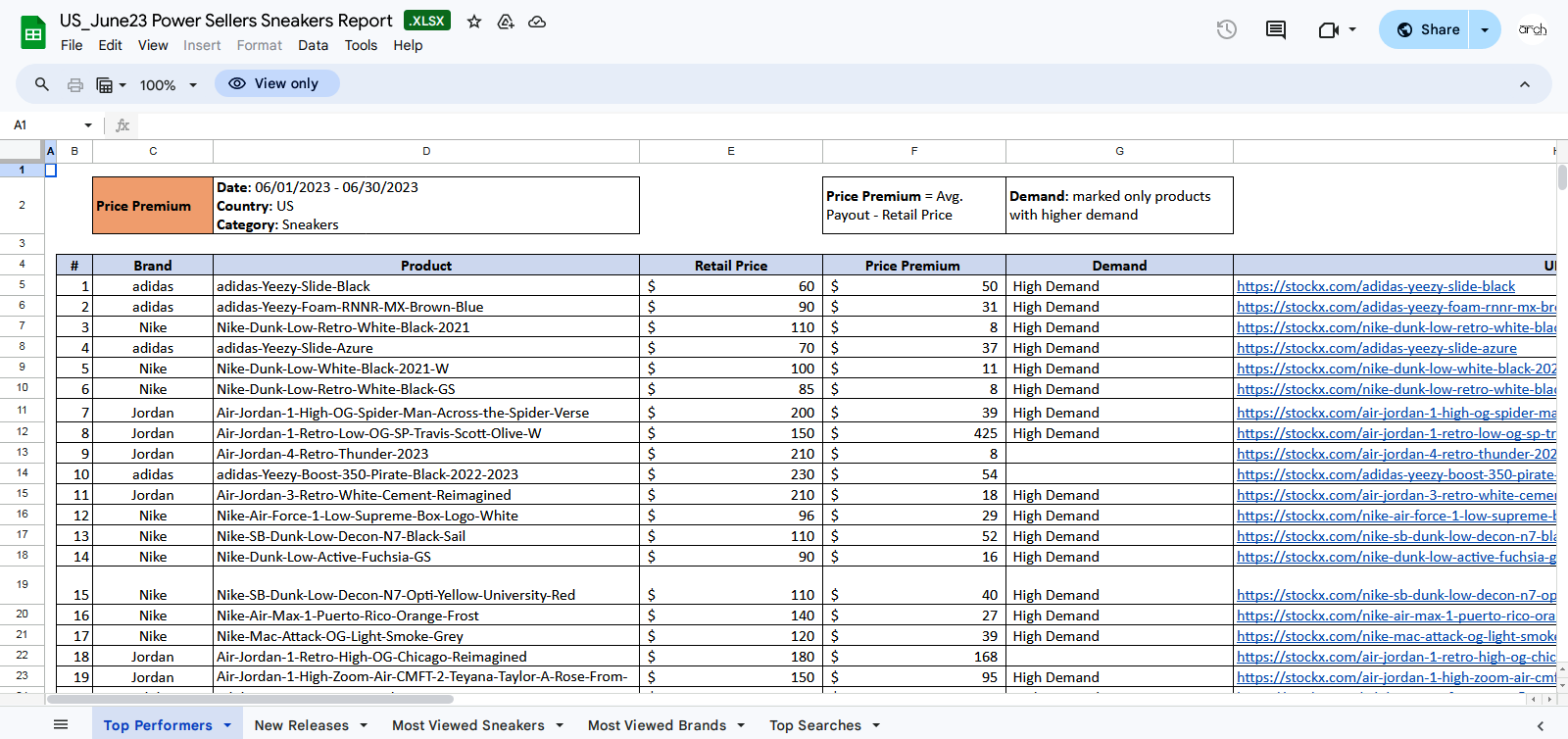

New Balance continues to be our fastest-growing core. The 9060 surpassed the 2002R in terms of volume to be the 2nd most popular model, with the 550 still being #1 (Note: The report by StockX states New Balance is the fastest growing. The reality is the top 19 sneakers sold in the picture below don’t include NB. The only model to actually crack the top 100 sneakers was the 990v6 Action Bronson Lapis Lazuli. What does this mean? If one sneaker sold in 2022 and two sold in 2023, that’s a 100% growth…)

Crocs has remained hot, driven by new Salehe Bembury releases. We also expect the Taco Bell Slides to continue to perform well into July/August (Note: There were three models of Crocs in the top 100 sneakers sold. They were all limited-edition models with only the “Lightning McQueen” garnering true profit. After fees the two other Crocs netted a small return.)

Converse pace has picked up, driven by below MSRP CDG collaborations. These items are included as hero items in our upcoming marketing campaigns, so we expect good performance in the coming months (Note: This note is telling and was a true predictor of resale returning to its roots. Not even a CDG collab could pull in an above retail value. As a matter of fact, the CDG was available at the Converse Outlet with an additional amount off which is why it was being sold below retail.)

While Nike and Jordan’s releases continue to be relatively weak, we are seeing increased interest in closet stock (items released >4 weeks in the past). All of the Top 10 most popular sneakers in June were in closet stock. (Note: Boom! This is how resale has always been. June 23 was also the month the Greater Fool Theory landed. Note in the picture below the three Panda Dunks, if purchased at retail, led to a loss for sellers although they show a profit. The only models with a solid ROI are limited, coveted hard to find models. The general release sneaker was no longer being bought out by new resellers looking to turn a profit. A look through social media will find countless videos of sellers discussing “bricks” shoes they bought in bulk with bots or by paying managers which tanked.)

ASICS has performed well, driven by GR models of the Gel Kayano 14. This is an opportunity for sellers with access, as they are selling around MSRP (Note: ASICS didn’t have one model in the top 100 and again, note the wording here, “sellers with access.” There has been a longstanding theory that retail accounts are dumping inventory on StockX. It’s understandable this conspiracy exists. According to Outlets Zone, there are 86 ASICS stores in the U.S. Traditional accounts don’t really carry ASICS, so arbitrage is difficult. Where could the pairs being sold at or below MSRP be coming from?)

Yeezy trades skyrocketed in June, led by the restocks at the end of May. With price points now favorable for buyers, it’s an opportunity for sellers to move units with pace for summer, particularly slides and runners. We expect more restocks in the coming months as adidas sells through their inventory (Note: Yeezy hit a wall in 2019 long before Ye and the Three Stripes divorced. The only models garnering resale have been the slides and to be honest, that’s because the retail price and resale price lands in the sweet spot of 75-120 dollars.)

There is a lot to pull from StockX’s statements and the data, but when compared Year over Year it becomes apparent how the market finally landed from the inflated lofty position of the post-Covid environment. When reading June 2024’s commentary keep the low-mid tier pricepoint in mind. In 2022 I wrote a report and discussed a term I coined Assisted Resale and Unassisted Resale. These labels allowed me to talk about sellers with access to sneakers at cost and how this allowed the majority of third-party prices to sit in the low-mid tier. At the time I took mid up to $150 dollars. I later adjusted this number down to cap it at 120 when writing the Ja 1 Report.

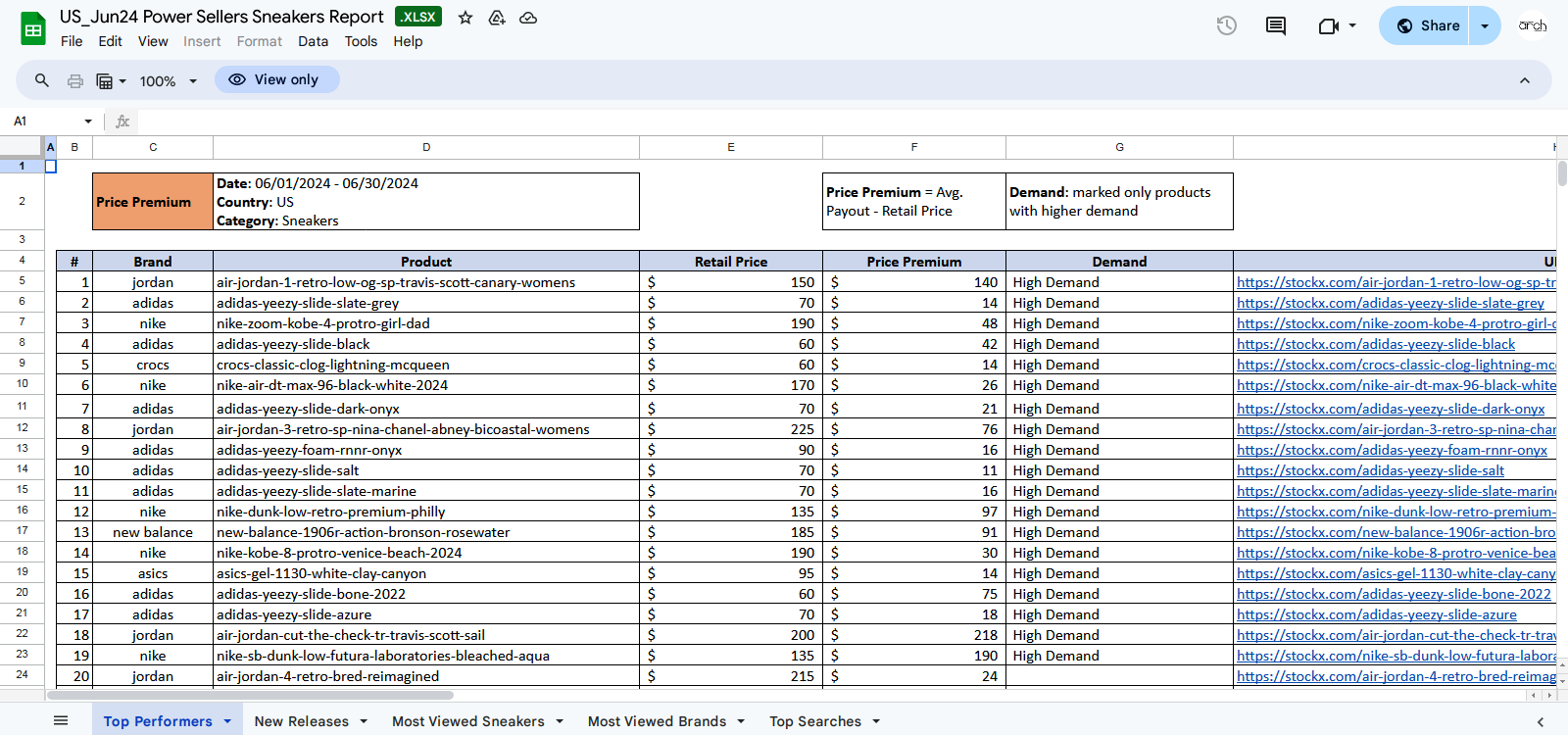

Yeezy trades continue to skyrocket following the June restocks, with the Slate Grey Slide being the #1 product on StockX in June. Prices remain profitable in all or most sizes, and volumes remain high as the warmest months of the year are upon us (Note: Once again, Yeezy is a limited drop, but so were the trainers. Those trainers, priced at 200 and higher, fell outside of the price consumers were willing to spend on kicks. Hence the increase of videos on social media of Yeezy sneakers being sold in adidas outlets at cost and still sitting. The slides in 2024 dominate the top 20 sneakers traded on StockX in June. Sneaker Resale is reverting to the Seller with the ability to hold inventory. As Yeezy Slides become rarer, the natural progression takes place. The new reseller who had been able to buy a Panda and flip it on the day of release doesn’t really have a business and I’m not certain that business model will return – which is unlike the cyclical nature of Sneaker Resale.)

ASICS demand continues, with June coming in as another record month for the brand on StockX. General release Gel-1130s continue to be the top movers, however, collaborations (like the Ronnie Fieg pack) also continue to move at high, profitable volumes. Onitsuka Tiger also continues to grow, driven by lack of supply for US buyers from retailers. (Note: ASICS in 2024 finally cracked the top 100 sneakers traded, but as StockX is stating it’s the limited drops which are profitable. The statement on Onitsuka is again the way resale used to work. That’s a good thing.)

AJ4s continue to move at a solid pace, with the Military Blue and Oxidized Green 4s coming in as top-traded products in June. We expect 4s to be a continued hot product, especially for fall and holidays. (Note: The Jordan 4 has always been a solid performer but note the top 20 Jordan 4 is only at 24 dollars average price premium. When you factor in the Reimagined 4 is 215 plus tax, the sneaker is being sold at a loss to the seller. The 4 does show up throughout the top 100 and the average PP is solid. Like traditional resale, the person with the ability to hold certain models will benefit.)

Within adidas, we are seeing a slowdown for Campus 00s. However, the Samba, Gazelle, and Spezial product lines are all continuing to grow. We expect this trend to continue in Q3. (Note: This note allows for an interesting dialogue about StockX and the opportunities the channel has. Do you remember the StockX x adidas IPO?

StockX has stopped utilizing the IPO program in a considerable way. They have barely used the DropX program. Why has the company seemingly forgot about two of its strongest features is unclear, but brands and retailers should both be looking back at those concepts and finding a way to implement the tactic into their repetoire.)

New releases from Crocs, namely the Naruto collection that was released in June, are trading at high volumes with most sizes being profitable for sellers. Crocs’ licensing collabs (Cars, Disney, Shrek, Spongebob) remain popular gifts for customers. (Note: Crocs should be careful. There is a harbinger in the data. In 2023 the Lightning McQueen had a PP of $136. The shoe was in the top 100 at 78. In 2024, the shoe is in the top 10 traded models on the platform and has dropped 90% in value to a PP of $14. This is the Greater Fool Theory in bright lights. The Crocs Juniper Guava Salehe is in the top 100 and performing extremely well, but if I had to guess this is a model in the B2B category – buyer to buyer.)

Sneaker Resale isn’t Dead

In Part 5 of this series a few of the things in this post will become clearer. Resale isn’t dead, it’s right where it’s supposed to be. A look at the data of New Release sneakers Year over Year will place into perspective how sellers are having to weather the cold temperatures since new releases are longer being snatched up by other sellers and consumers are no longer “pressed” to buy the latest drop. The question is how will this return to form shape retail during the holiday season? Every year the Black Friday, Jordan 11 and Christmas drops inspire sell through rates and help stores recover from the regular season. How will things work this year?