![]()

StockX is a private company with a massive amount of fundraising under its belt. The company is moving into a position where there won’t be another funding round. The company will have to IPO. In the first post in this series, I explained why the platform implemented guardrails to offset a slow market. Throughout this series I’ve attempted to explain how resale has cooled and why. It’s critical to provide data from StockX to show how the market is finally in its correction phase. First, however, context is required and more history.

New Releases have always been interesting to track. They offer insight to how resale has changed year over year. When I started the “Should You Buy to Flip” series no one in sneaker media was doing this. I created a formula which allowed me to choose which new sneakers I could use to gauge brand heat. When I turned the series over to Housakicks, a site created by a mathematician, he developed a stronger method of rating kicks. Today, every major sneaker YouTuber is attempting to analyze new releases, although the newer sneakers aren’t hitting they were three years ago.

In StockX’s State of Resale 2024 they stated:

“The sneaker resale market isn’t dead: Despite headlines claiming otherwise, StockX data shows a diversified portfolio of brands that are locking in the top spots for year-over-year growth including Asics (+589%), adidas (+88%), and Yeezy (+23%). The latter depicts the complexities of shopper behavior, where virtue signaling falls to the wayside, in favor of cultural clout. The sneaker resale market for the usual top-charting mainstream brands like Nike and Jordan however has slowed, as market share has dropped 11% and 12% respectively from 2023 to 2024.

Sneaker innovation is king: The days of relying on one silhouette no longer drives heat across an entire brand. The Nike Dunk, as an example, formerly reigned supreme, but data shows a dip in popularity with trades down 41% year-over-year. Similarly, cornerstone silhouettes from brands like Jordan and New Balance have dropped in average price, such as Jordan 1 (-18%) and New Balance 550 (-25%). Conversely, Asics, which has reimagined its older silhouettes such as the Gel-1130 and Gel-Kayano 14, have seen a huge increase in growth on StockX (+589%).

Celebrity athletes for the win: Signature sneaker lines helmed by legacy NBA giants Kobe Bryant, LeBron James, and Kevin Durant drove Nike Performance Basketball, up 46% year-over-year. The mamba mentality starts in the sole with the Kobe Protro in the lead with a 512% trade increase, followed by Devin Booker’s Book 1 (+14K trades this year-to-date with a +18% price premium) and KD (+6K trades this year-to-date). The WNBA is also heating up with superstar Sabrina Ionescu’s signature Sabrina 1 silhouette (+3K new trades year-to-date) garnering new attention relative to launch.

The days of relying on one silhouette… this is the most important line in the statement above and is a direct shot at Nike and the Dunk and Jordan and the Air Jordan 1. Prior to StockX’s arrival, and by default GOAT, Grailed and other digital resale platforms, resale required a more thoughtful approach. Sure, there were sellers who knew the Jordan 11 was going to pop, or the Black Friday drop would perform well, and those sellers had the money to buy as many as possible… but true businesspeople relied on a more nuanced approach involving a diverse product mix. Remember, the reseller at one point was additive to the market. Revisiting the time before StockX can offer a foundation to this discussion before moving forward with data from 2023 and 2024.

Revisiting the Curry 3

In 2016 StockX was in motion, but the site was a sliver of what it is today. Sellers had to utilize Amazon, eBay, Kixify or other consignment shops like Stadium Goods and Flight Club. Sneaker Reselling was speculative, but it was more of a business. It required planning, purchasing, customer service and handling returns. New releases were truly like initial public offerings as sellers were at the mercy of the market and the seller relied on brands to create interest for a release. Sneaker blogs were important, but purchasing decisions remained a function of the marketing strategy of the companies making the kicks and the distribution strategies since not every area in the U.S. received allotments of certain kicks.

Under Armour’s Curry 3 provides an interesting look into how a new release could perform on the third-party marketplace. When looking at the Curry I looked at a few metrics:

- The brand was coming off of the loss of The Sports Authority.

- That bankruptcy left UA looking to create more accounts.

- This didn’t happen quickly.

- The Curry 3 wasn’t a hyped release.

- Under Armour was overlooked.

- Resellers didn’t even think about the brand as an option.

- Only sellers who actively worked in retail, resale and wholesale knew there was an opportunity. I saw the fact that Under Armour wasn’t available in many retail outlets, so I began to acquire the Curry 3.

- Steph was a champion and there was demand, but Under Armour had reduced the amount of advertising for Curry’s shoes. They had just faced the “Chef Curry 2.5 debacle” and the brand basically left the sneaker in the hands of Curry’s basketball career.

I mention this to establish that new releases in resale had a place, but only when a number of circumstances came together. This was unlike the post-Covid resale boom where every Dunk and Jordan 1 Mid or Low hit resale numbers. My purchase of Curry 3 shoes at SRP was a very calculated plan which relied on poor distribution. I live in a Nike crazy city, so the Curry 3 wasn’t selling at all. I was able to move the new release without disrupting the market by monopoly.

Do Not Pass Go – Monopoly

2023 saw the resale market come back in alignment with pre-StockX. The early years of resale had moments when new releases could pop and become profitable overnight, but resale was a matter of relationships and knowledge. If you didn’t have the right connections or a deep knowledge of the market, reselling wasn’t easy to pull off. There was considerable risk. The Concord (2011) and Nike’s Galaxy Pack (2012) changed things drastically. Sneaker Resale became less about finding deadstock in storerooms and turned into monopoly for deep pocket players. The Nike Yeezy era arrived and there was FOMO settling in. As I mentioned in Part 3 of this series, pay to play was ridiculous. The backdooring became disruptive but there were still opportunities in sneakers people didn’t realize had limited distribution.

I focused on an array of sneakers from the adidas D Rose, which was a poor performer in Memphis although Rose went to college here, and I also found that the Chinese market didn’t have the same access to Jordans. For years GS sizes were easy to move via Amazon, more on China in a few paragraphs.

After the Galaxy Basketball pack, Nike Basketball began to decline. Nike, as they have done in today’s market with the Dunk and Jordan 1, inflated their retail pricing with Elite options that took KD, Kobe and LeBron sneakers from the 120 to 250 dollars. (The Elite Signature Pack pictured below)

Ain’t No New Thang

Nike’s price inflation on items which popped in resale has always been a thing. In every instance, the Swoosh killed its market. The Elite Pack options ended up on discount at Nike Clearance and Factory stores. While the lifecycle of the product was still 90 days, when the shift from performance to casual sneakers happened, Nike didn’t seem to take notice. This opened the door for adidas and their better priced options to take off. This should sound familiar.

The ZX Flux was adidas’ answer to the Roshe. Kanye moved from Nike to adidas, and the 90 – 110-dollar pricing allowed the Flux and NMD to take off like a rocket. Nike was still pushing inflated priced basketball and failed to recognize the seasonality of performance basketball (which still sold, but much slower than in the past). Nike was in the beginning stages of Nike Direct and the Consumer Offense. There wasn’t a name for their direct-to-consumer strategy, but Nike started to force smaller store accounts to take on Nike Basketball and underperforming Jordan Brand in-line models.

Jordan Brand bought into its prowess and dumped Jordan 6 Lows into the market and Air Jordan 1 Lows. Almost all of this product by 2015 was sitting, but new releases from adidas, the UltraBoost, dropped into the resale arena. adidas was gold until the brand followed Nike. They bought into their own hype and inflated pricing of the NMD from 110 to 180. They broke their own success and gave all of their North American business over to YZY.

History

Why is this history necessary when discussing the Year over Year of New Releases on StockX? In Part 1 I gave a list of “valve restrictions” which caused resale to explode. I explained that resale was a crack in a tight pipe. StockX’s rise in popularity in 2017 gave many analysts proof of the growing resale landscape. I always argued that growth was a leak in a wide pipe. The arrival of StockX and GOAT brought new players into the business of resale, but it had become harder to operate an online shop as New Releases made Sneaker YouTube a new form of marketing. Having a sneaker early allowed for credibility. New became the trend. The sneakers which could be bought on discount began to see diminished returns and acquiring new sneakers, which were reselling, got harder as those GS buyers from China began to send teams to the U.S. to acquire inventory. The scramble for inventory began.

The New Release grew in value and buyers began buying from buyers. Consumers began to grow jaded. The tone around taking an L on SNKRS went from a badge of honor to an irritant. This opened the door for smaller brands. The New Release fell out of favor. The GS market collapsed because Nike went all in on China and flooded the market there. Buyers for the POIZON app no longer needed to fill containers to ship back to China. The bubble popped and as StockX wrote in the report above, relying on one style no longer carries a brand. History has seen sneaker resale move back into a narrow pipe, but I don’t think that will happen again. Nostalgia doesn’t drive interest and being a sneakerhead isn’t as cool anymore.

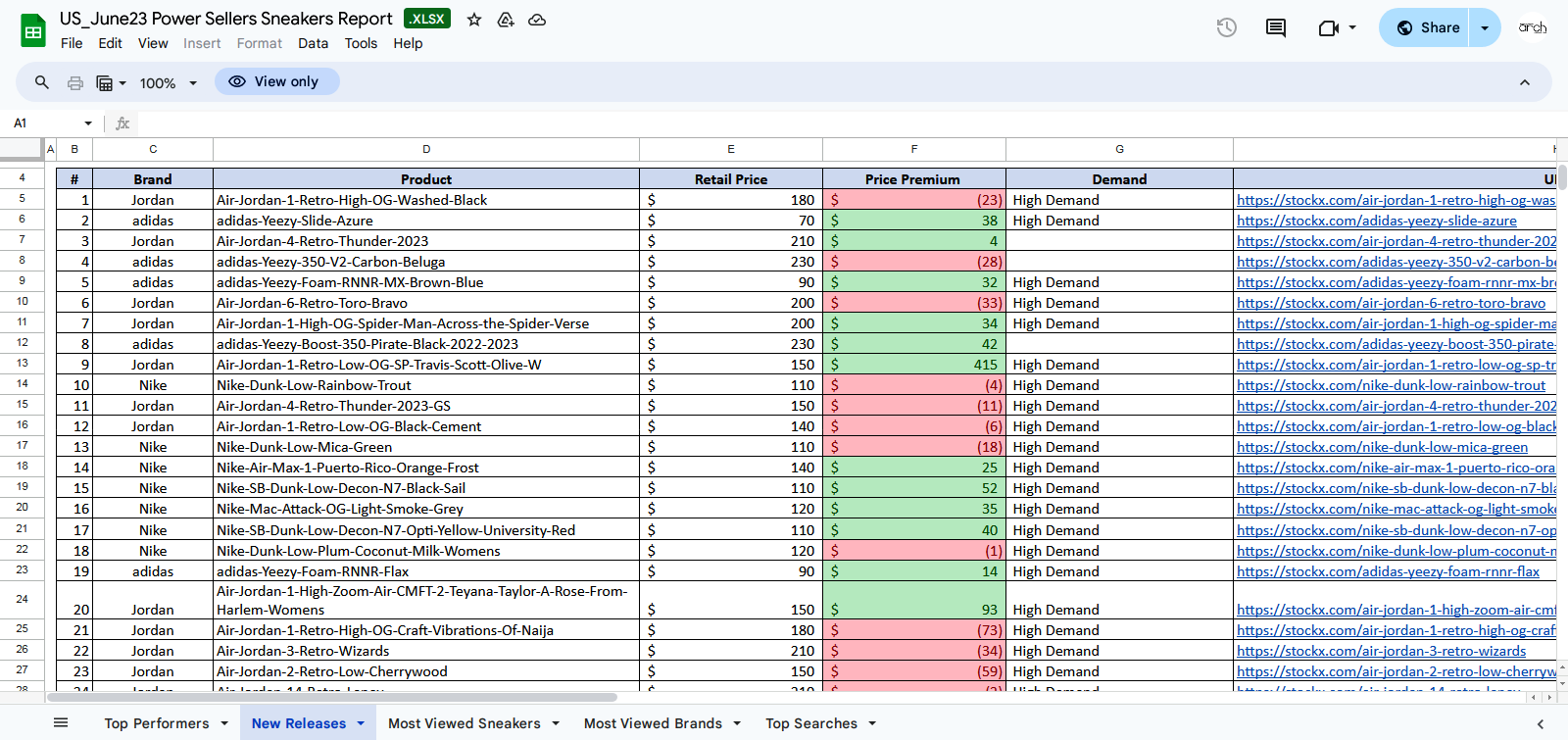

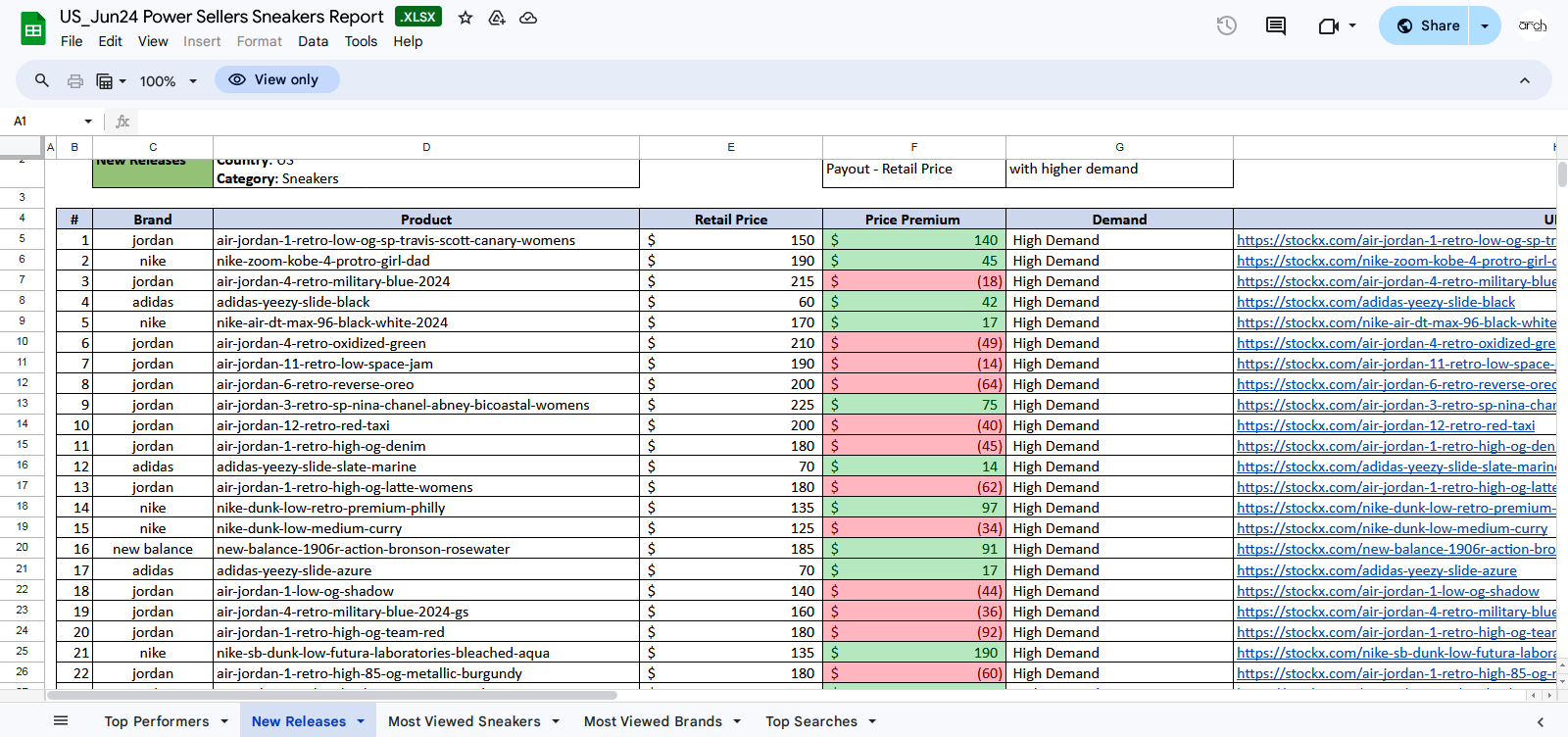

2023 vs 2024 New Releases

Take a look at these two slides from June 2023 and June 2024. What do you see? There is a lot here and it requires a lot of math which is better seen in charts. Looking at the top 22 sneakers year over year provides considerable context.

- 10 out of 22 new release sneakers in 2023 were in the red. 12 out of 22 new release sneakers were in the red in 2024.

- The price premium from all profitable new releases in 2023 was $824.00. The price premium from all profitable new releases in 2024 was $728.00

- The average depreciation on new releases in 2023 was -$23.10. The average depreciation on new releases in 2024 was -$46.50

- The best performing new sneakers in both years were limited release kicks (this is to be expected).

- In 2023, three of the depreciated new sneakers had single digit losses. In 2024, every new sneaker which depreciated took double digit losses.

- A new release Air Jordan 1 is a like a car driving off the lot, unless it’s a Travis Scott, but even the 2024 Travis Scott’s value is greatly diminished compared to the value in 2023.

There are so many data points to look into and StockX provides a unique resource for those willing to mine the data. New Releases, to be honest, should have never been a part of the natural lifecycle of product releases… at least not in the way things took shape. When buyers began paying store managers for new releases, when sellers began using bots to snatch up inventory of popular sneakers, the inevitable breakdown of the resale market was scheduled.

Resale can be an additive process for clearing inventory. Resale is important in helping buyers in under distributed locations attain the sneakers they want. The last two years have seen a return to what resale was, kind of. The genie is out of the bottle and the business of kicks has changed, but there are ways to right the ship. Do I think this industry is capable of understanding the cool down which is important in recovery? Not really. I think every brand will discuss scarcity and reducing the number of particular models, but they aren’t really clear on why kicks have diminished in popularity and until they treat the roots, the roses will have spots.

Read this Series

StockX Adjustments in a Cooling Resale World – Part 1

The Death of FOMO in Sneaker Resale – Part 2

Made to be Discounted and the Arbitrage Snitch -Part 3

How the Year over Year Reports on Resale Provided Hints of the Reality – Part 4