![]()

Morris A. Modell opened his first store on Cortlandt Street in Lower Manhattan in 1889.

Source: Modell’s Sporting Goods to Close All Stores After Bankruptcy Filing

When I began writing the book Nike’s Consumer Direct Offense, Amazon & StockX: The Disruption of Sneaker Retail, I floated back and forth on placing “sneaker retail” in the title. The book relates to any industry relying on wholesale accounts with brands. In 2014/2015 I began documenting the closure of mom and pop shops in my region as bigger chains like The Sports Authority went bankrupt, and Finish Line began closing a considerable number of stores. One of the biggest issues I had in discussing these things was that my reach was very small. I decided to start following and engaging with people in the industry like Matt Powell and his NPD Group. They were the only people being interviewed by large news outlets and showing up on shows when the sneaker industry was discussed.

I reached out to Powell and was ignored and told that I was wrong about everything I was discussing. I soon realized that speaking with Powell was futile as the reality of what his information was had very little to do with the reality taking place for retail locations and for myself. I wrote this post to explain that the data wasn’t being read correctly in resale:

I continued to look to Powell for answers, but soon realized the majority of information shared was based on data from previous quarters. This didn’t help me in my quest to find out more about why my own numbers were dwindling or why the stores in my region and across the country were closing. I continued writing and in 2016 I was blocked by Powell and I began challenging his information by doing a lot of independent analysis and investigating. I still didn’t have a very big following, so I wasn’t reaching enough people, but this post below became the turning point for me listening to people who crunch numbers but aren’t actually living and breathing the business:

Why You Should Question NPD’s Data About adidas Overtaking Jordan Brand

In this post I delivered this analysis:

Nike’s DTC grew from

2014 (768 Nike stores)

2015 DTC 6.6 Billion (832 Stores)

2016 DTC 7.9 Billion (919 Stores)

2017 DTC Revenue 9.1 Billion (985 Stores)

Now, I repeat I don’t know the source of Powell’s data. What I do know is that Nike grew the number of their physical stores from 919 to 985 stores since 2016. THIS IS IMPORTANT: I don’t need to know Powell’s data to understand that as Nike grew e-commerce, and in store sales via Nike Factory, Nike Clearance and Nike Employee Stores that the natural progression for Nike footwear at retail would be a decrease in sales.

Has adidas taken shares of the retail market from Nike? YES

Did Nike lose money overall last year to this year? NO

A few FACTS from Nike’s last quarterly report:

• Fourth quarter revenues up 5 percent to $8.7 billion; 7 percent growth on a currency-neutral

basis*

• Fiscal 2017 revenues up 6 percent to $34.4 billion; 8 percent growth on a currency-neutral

basis*

• Inventories up 4 percent as of May 31, 2017

I wrote all of the above to establish that there is a parallel that can be drawn to the consistent closure and acquisitions taking place in sneaker retail. Right now a journalist is looking to quote someone and they will look only to one person and in turn the problems taking place in the industry will continue because only one voice is being heard and listened to. Journalists are going to have to work harder. There are a bevy of sources available consisting of people on the ground floor. I was able to engage with an extremely knowledgeable store manager who once worked with Modells on LinkedIn recently. The topic was Modells:

In this back and forth a number of people chimed in, but I explained in so many words that Modells was the outcome of an unwarranted surgery. Nike’s Consumer Direct Offense, Direct to Consumer strategy, was not needed. It was a cosmetic surgery that improved the beauty of the company for shareholders, but is and remains the biggest threat to the retail industry. As Nike goes, so do other brands. With all brands touting growth via DTC the ONLY natural progression for retail outlets is atrophy.

In the Times article Joseph Favorito is quoted as saying, “Heard a company exec the other night blame losing teams in NY as part of the reason; in reality a failure to adapt to a new economy & delivery system is the reason.” His commentary was about Modells and the owner’s comment that sports teams on the East Coast was a factor in their failure.

Favorito is wrong. Greg Garber, quoted above from the LinkedIn dialogue was a manager at the chain. He stated, “In-store Modells utilized a stock locator system that included a tablet which allowed the manager to engage with the consumer on the spot. If the size wasn’t in inventory, using the tablet the customer could have their selection shipping directly to their home.” This is a system that Foot Locker only recently began utilizing with handheld scanners and Foot Locker still doesn’t have tablets. They can only check inventory on the floor and they have to take the additional step of moving the customer to the register to complete the sale. While Foot Locker has long been using Stock Locator, how was Modells failing to adapt when they were more advanced?

Modells created a robust e-commerce site and they utilized social media to drive engagement. Their YouTube was at almost 5,000 subs over ten years. That’s not great, but they were creating content. 183,000 fans followed them on Facebook. They have 58,000 followers on IG and on Twitter they had 25,000 followers. Their website was garnering 2 Million visits a month at the holidays and 1 Million today. This is comparable to other small chains, but there is a considerable difference when compared to other small chains. Modells does not receive high end sneakers. Modells isn’t an urban account. There aren’t any Jordan Retros, or Yeezy to pull in online sales. Why is this important? They did everything right for their market. To grow digital Modells would have to had an account that included hyped footwear. That’s really the biggest problem for the store. It wasn’t that they failed to adapt, they operated in a traditional retail space that was undercut by the main brand that provided them with footwear and apparel.

When Modells started selling team sports gear Nike didn’t own the uniforms for the MLB, NBA, and NFL. Modells’ reliance on sports jerseys was a positive. In the last three years however they weren’t competing against Pro Image or Mitchell & Ness. They were in direct competition with Nike and Nike sells their products at a higher clip than any other retailer. Nike uniforms feature Nike Connect. Fans can listen to their favorite players’ playlists or get information on the team by scanning the jerseys. That’s a cool feature, but the most important feature for Nike is that scanning the jerseys takes the buyer into the Nike digital ecosystem where fans of the brand spend 3Xs as much than they do at brick and mortar. Nike implemented QR codes. Shoppers in Modells could scan a jersey and get a better price on the Nike website. The QR codes were added to all footwear as well.

Modells was also fighting a robust resale environment that advertises and captures sneakerheads. Sneakerheads are no longer niche, it’s mainstream with more people participating in the culture than ever; including kids with parents who would have once taken their kids to Modells for a great deal on sneakers. As sneaker culture has become mainstream, third party e-commerce has become a billion dollar industry creating new competition for Modells with better product. GOAT is connected to the NBA and Foot Locker. StockX is connected to the NBA, advertising on national sporting events, and is doing partnerships with adidas and other brands for drops directly on their digital site.

Modells is selling sports equipment at a time when kids are getting into eSports and participation in sport is declining considerably. Modells was being pushed from every angle. They didn’t die because they failed to adapt. They failed because every brand they carry decided to get cosmetic surgery in the form of DTC and shift the entire retail industry. Nike didn’t need to go directly to their customer, but you can’t blame them… it’s great for their shareholders.

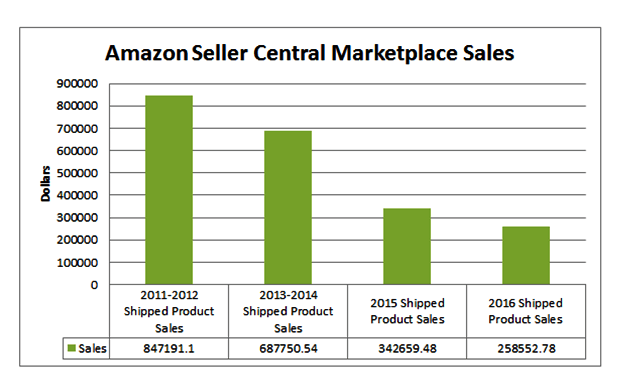

I’m sharing my sales chart from 2011 to 2016. I operated as a third party seller on Amazon Seller Central. I began writing more informative posts on this site because of what you will see below. This isn’t the POS for the entire industry. These are mom and pop numbers. They were immediate reflections of what was happening in the sneaker industry:

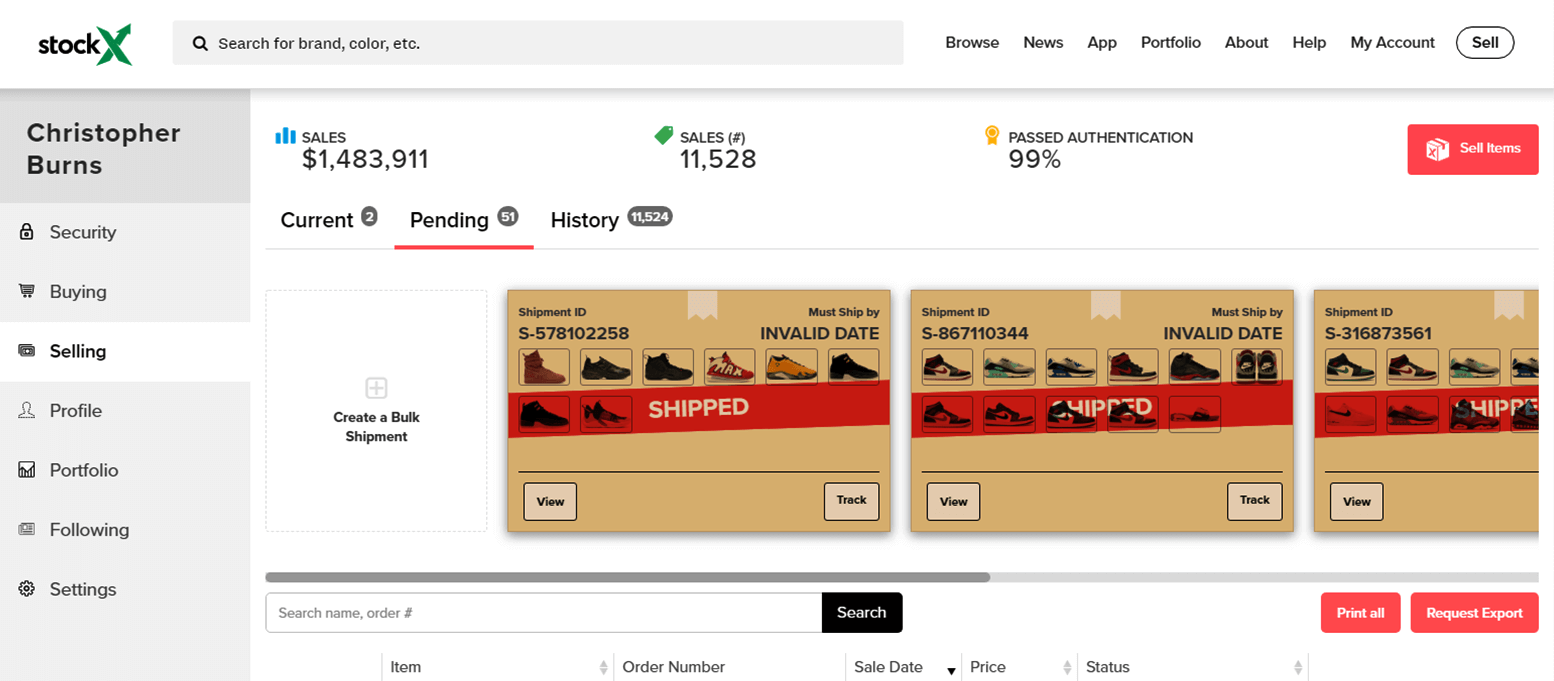

I’m sharing my sales data from the last two years utilizing StockX. This is real time and not POS data from three months ago or a previous quarter. These numbers are updated daily. These numbers are why eBay decided to remove seller fees on sneakers above 100 dollars. These numbers are why adidas decided to work with StockX to do a limited release of sneakers not through a retail partner, but through the digital site itself.

Could Modells have adapted?

Yes.

Why didn’t they?

Why didn’t The Sports Authority? Why did Finish Line induce a poison pill before selling to JD Sports? Why did City Gear have to sell to Hibbett Sports? Why did DTLR and Villa have to join forces?

Retail has at its disposal a network of people to consult with, but if they all started at one place the dialogue would begin. The store manager is a daily source of information readily available, but underutilized due to an antiquated system of hierarchy. POS data from previous quarters does not tell the story fast enough to inform C-suite and upper management of the shifts required to adjust appropriately. The entire industry relies on reports from companies built on data that doesn’t report in real time. Modells is the face of the reality of direct to consumer strategies for the moment. In a few months another face will appear and we will repeat this process while families will suffer the consequences of Nike, adidas and other brands continuing to move closer to their customers without any middle men.